Monthly Market Snapshot – July

Stocks rose in June, wrapping up a quarter marked by an AI-sparked tech rally, surprises from hawkish central banks, and signs of weakening economies. The S&P/TSX Composite Index and S&P 500 Index posted gains for the third consecutive quarter, while U.S. small caps underperformed large caps due to lower earnings and exposure to cyclical sectors. In fixed income, global high yield outperformed Canadian and global investment grade bonds.

Canada’s benchmark S&P/TSX Composite Index was up 3.0% in June and posted a 0.3% gain for the second quarter of 2023. Four of the benchmark’s underlying sectors were positive during the quarter, led by information technology with a 16.5% return. The materials sector was the largest detractor for Q2, with a decline of 7.4%. Small-cap stocks, as measured by the S&P/TSX SmallCap Index, fell 5.2% for the quarter.

The U.S. dollar depreciated by 2.0% versus the loonie during the quarter, slightly dampening the returns of foreign markets from a Canadian investor’s standpoint. Note that all returns in this paragraph are in CAD terms. U.S.-based stocks, as measured by the S&P 500 Index, rose 3.5% in June, and finished the quarter higher by 5.9%. The benchmark’s quarterly gain was led by information technology and consumer discretionary, with respective returns of 14.4% and 11.8%. Utilities and energy were the main detractors for the quarter, declining by 5.4% and 3.9%, respectively. International stocks, as measured by the FTSE Developed ex US Index, fell 0.1% during the quarter, while emerging markets declined 2.6%.

The investment grade fixed income indices we follow posted mixed returns in Q2. Canadian investment grade bonds, as measured by the FTSE Canada Universe Bond Index, were down 0.7% during the quarter. The key global investment grade bond benchmark was down 1.5%, while global high-yield issues rose 1.6%.

Turning to commodities, natural gas rose 26.3% in the quarter, while the price of a barrel of crude oil shed 6.6% in the same period. Gold, copper and silver all had a negative quarter with respective losses of 2.0%, 8.6% and 5.6%.

Inflation in Canada was 3.4% year-over-year in May, from 4.4% year-over-year in April – the lowest level since 2021. On a monthly basis, the index rose 0.4%, on par with expectations. The Canadian economy lost over 17,000 jobs in May, as the nation’s unemployment rate rose to 5.2%. The Bank of Canada raised its key interest rate to 4.75% in June, ending the conditional pause that started in January.

U.S. nonfarm payrolls rose by 339,000 in May and the unemployment rate climbed to 3.7%. The consumer price index increased 4.0% year-over-year in May. Shelter, used cars and motor vehicle insurance all contributed to the monthly advance. Meanwhile, airfares and household furnishings declined. The Federal Reserve held the federal funds rate to a range of 5.0–5.25% in June, following 10 consecutive increases since March 2022.

Chart of the Month

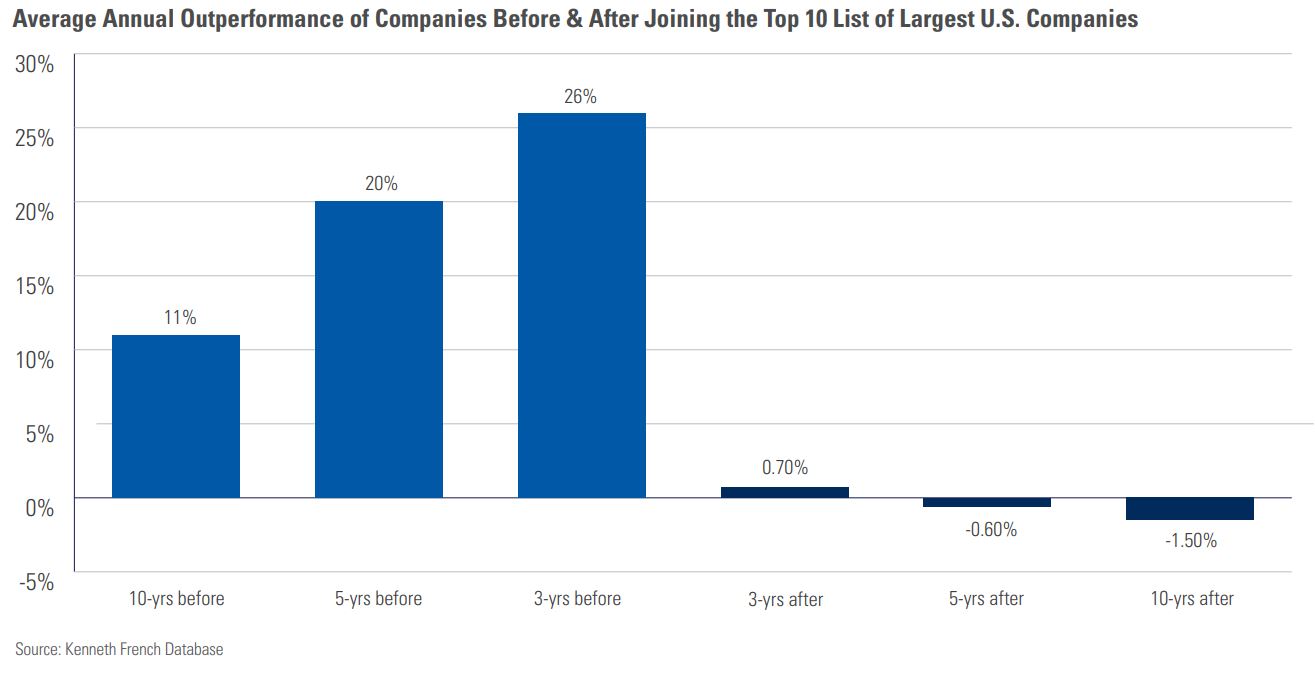

Most investors view large, established companies as a sound investment choice, as they’re generally considered less risky than small- or mid-cap names and they often pay dividends. However, the top 10 largest companies in the U.S. tend to underperform the overall market for the five-year period after entering this elite group. In the three-, five-, and 10-year periods prior to joining the top 10, the performance of these companies has been exceptionally strong, which makes sense given that in order to reach this pinnacle, they would have to be growing faster than the current set of top 10 companies. From 1927 to 2021, the average annualized outperformance for top 10 companies three years before joining the list was 26%. However, after three years in the top 10, outperformance against the market was less than 1%. After 5 years, the mega-cap stocks start falling behind the market by 0.60%, with the gap widening to 1.5% after 10 years. For investors, this shows the diminishing returns associated with investing only in the largest companies in the U.S., despite their historically lower risk and volatility. It also suggests investors would do well to gain exposure to companies that are on a clear path towards becoming a top 10 name.

Posted In: Market Updates